Finland’s 2027 Licensing Reform and Nordic Market Entry: A Guide to Regulation, Certification, and Content for Operators, Suppliers, and Investors

Data current as of June 2026. Regulatory frameworks continue to evolve. Verify regulatory requirements before committing to market entry, particularly in Finland, where implementation is ongoing.

What You Need to Know in 90 Seconds

| Country | Status | Your entry path | Priority |

|---|---|---|---|

| Finland | Opens July 2027 | B2B licence from July 2027, mandatory from Jan 2028 | Now |

| Denmark | Licensed since 2012 | Supplier certification required since Jan 2025 | High |

| Sweden | Licensed since 2019 | Gambling software permit required since July 2023 | High |

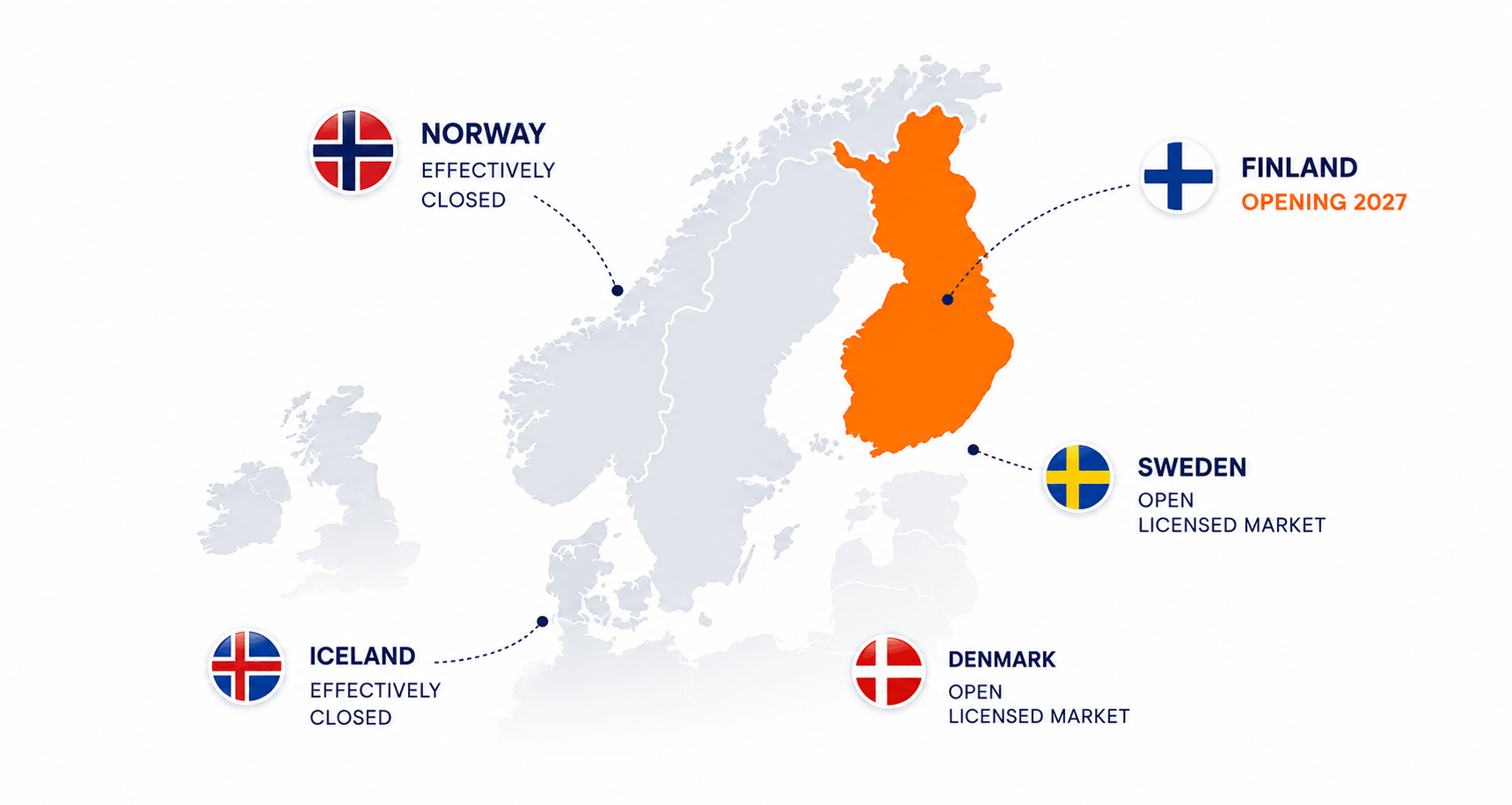

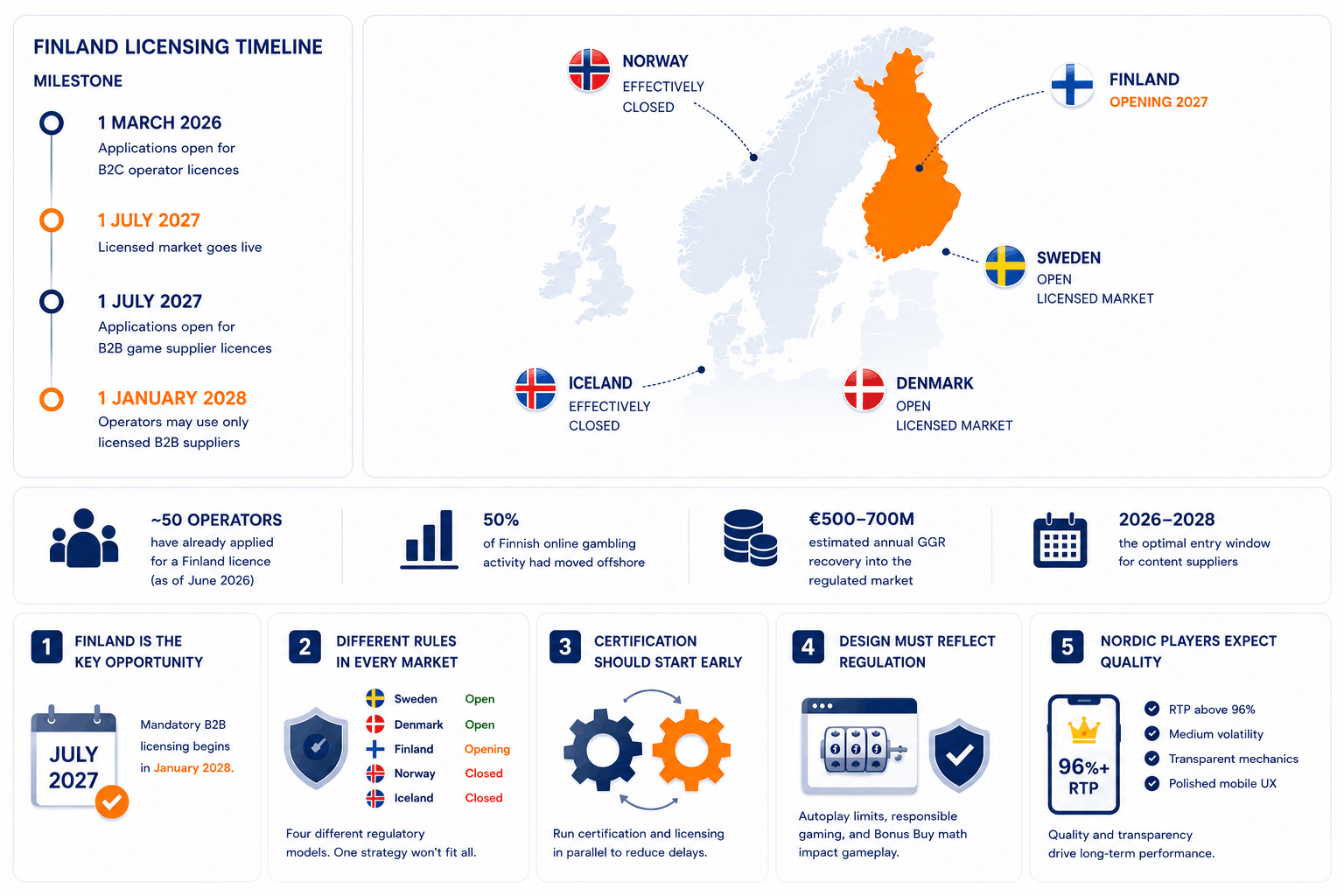

| Norway | State monopoly | No commercial entry available | Monitor only |

| Iceland | Restricted | No commercial entry available | Skip |

Finland is the window. Before the reform, Finns wagered an estimated €520–590 million per year on unregulated offshore platforms, around half of all online gambling spend.¹ As of June 2026, roughly 50 operators have already applied for licences.² Catalogues are thin. Suppliers that certify early get placed first.

Three facts that change the production plan regardless of which market you enter:

- Autoplay is banned or tightly restricted in Sweden and heading the same direction in Finland.³ The base game must work without it.

- Bonus Buy faces regulatory and operator pressure across the region. Games dependent on buy-feature revenue have a structural problem here.

- Nordic players check RTP. The effective floor is 96%. Below that, a title loses visibility before a player ever loads it.

Why Finland 2027 Matters

For years, Nordic expansion meant entering two mature markets, Sweden and Denmark, while accepting that Finland and Norway were closed. That changes between 2026 and 2028.

Finland is replacing the Veikkaus monopoly with a licensed online gambling market. Unlike Sweden, where suppliers compete in a saturated ecosystem, Finland opens with a thin catalogue. Operators entering the market will need certified content from day one, and the suppliers already in their portfolios will be first to benefit.

Online slots account for approximately two thirds of casino-segment betting in Finland.⁴ The content opportunity is direct.

Finland Licensing Timeline

| Date | Milestone |

|---|---|

| 1 March 2026 | Applications open for B2C operator licences |

| 1 July 2027 | Licensed market goes live |

| 1 July 2027 | Applications open for B2B game supplier licences |

| 1 January 2028 | Operators may use only licensed B2B suppliers |

The structure creates an unusual transition period. Operators can begin preparing for launch before B2B licensing becomes mandatory. Suppliers that complete certification early can position themselves for catalogue inclusion before the market reaches full maturity.

Another reason Finland attracts industry attention is channelisation. Before the reform, Finns wagered an estimated €520–590 million per year on unregulated offshore platforms, around half of all online gambling spend, and nearly 90% of that offshore turnover came from just 6% of players in the high-risk group.¹ Recovering that spend into the regulated market is a central goal of the reform.

Industry interest has been immediate. By June 2026, approximately 50 operators had already submitted licence applications, signalling strong confidence in the new market.²

Early catalogue placement in 2027 will be materially easier than entry in 2029. The window is real and it is time-limited.

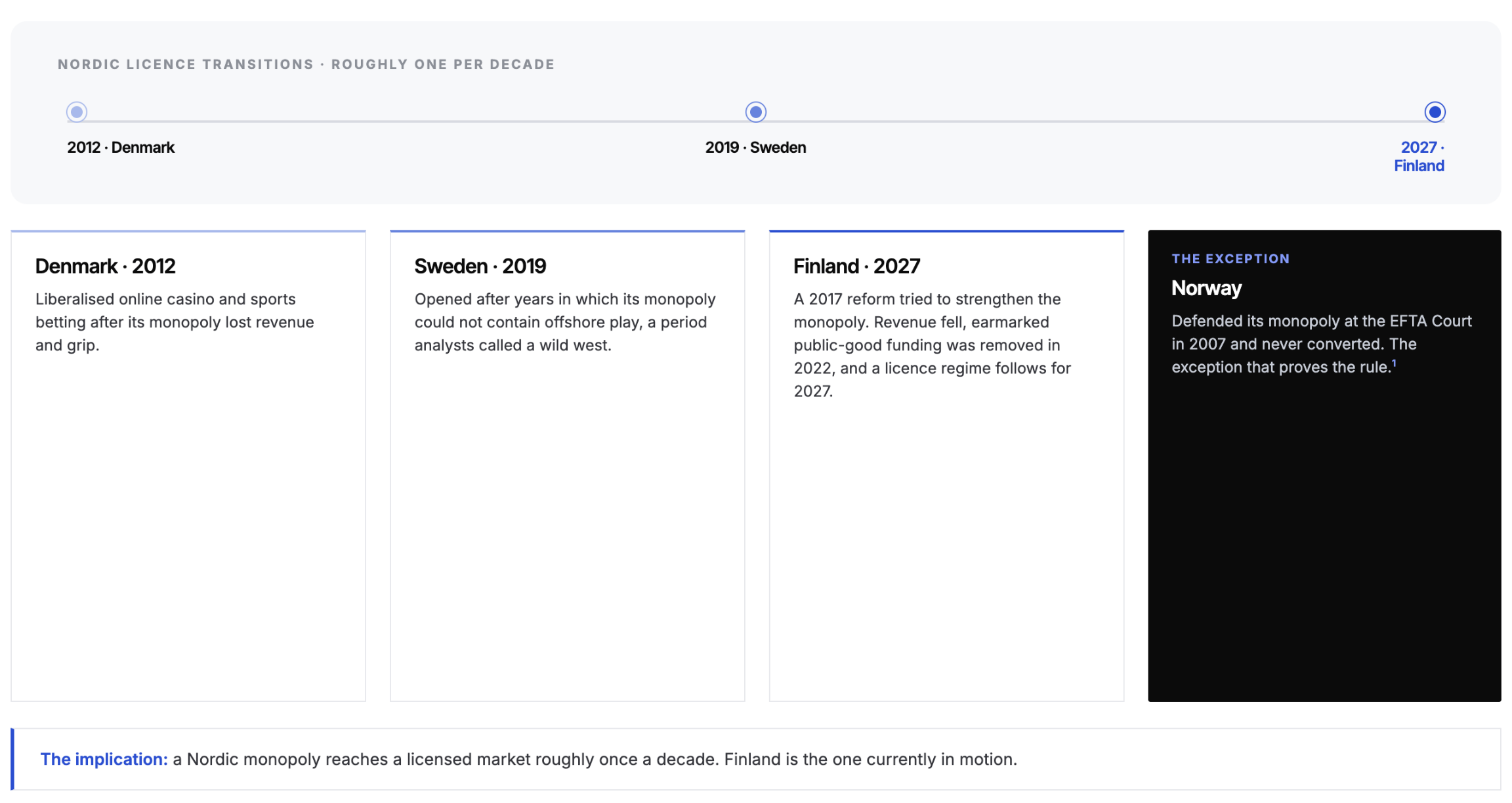

Why the Monopolies Fell

Finland is not an isolated event. It is the latest step in a twenty-year Nordic pattern, and understanding that pattern is what makes the timing credible rather than promotional.

Academic analysis of Nordic gambling policy shows that each licence transition followed the same trigger: not political preference, but the collapse of monopoly market control.⁵ Denmark liberalised online casino and sports betting in 2010 (extending to bingo and horse betting in 2017) only after its monopoly lost revenue and regulatory grip. Sweden opened its licensed market in 2019 after years in which its monopoly could not contain offshore play, a period contemporary analysts described as a “wild west.”⁵ Finland followed the same arc: a 2017 reform tried to strengthen the monopoly, a player-identification requirement and the COVID-19 closures cut revenue, and by 2022 the state removed gambling’s earmarked public-good funding. When measures to reassert control proved ineffective, Finland moved to a licence regime, enacted for a 2027 opening.⁵

Norway is the informative exception. It defended its monopoly successfully before the EFTA Court in 2007 and has spent two decades reinforcing it.⁵ Norway is not “closed for now.” It is a deliberate, durable monopoly, and studios should plan accordingly.

A Nordic monopoly reaches a licensed market roughly once a decade, and Finland is the one currently in motion.

Nordic iGaming Is Four Different Markets. Regulatory Overview by Country

One of the most common planning mistakes is treating the Nordic region as a single regulatory environment.

It is not.

Although the countries share similar player expectations and high digital adoption, their licensing systems, technical requirements, and supplier obligations differ substantially. A single Nordic strategy is, in practice, four separate regulatory projects.

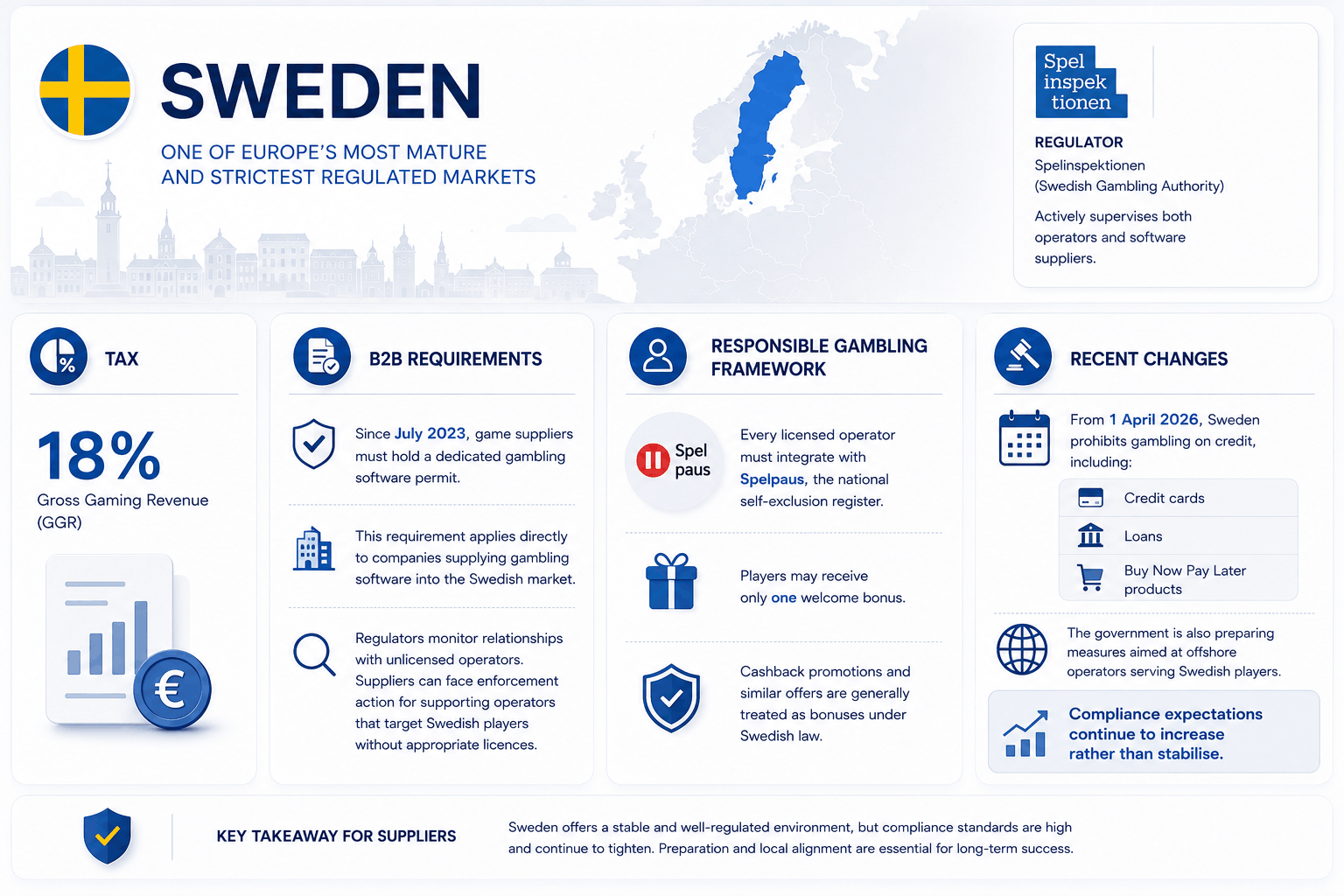

Sweden

Market Status. Sweden has operated a licensed gambling market since 2019 and remains one of Europe’s most mature regulated jurisdictions. For suppliers, it is also one of the strictest. The Swedish Gambling Authority, Spelinspektionen, actively supervises both operators and software suppliers.

Tax. 18% Gross Gaming Revenue (GGR).

B2B Requirements. Since July 2023, game suppliers must hold a dedicated gambling software permit. This requirement applies directly to companies supplying gambling software into the Swedish market. Regulators also monitor relationships with unlicensed operators: software suppliers can face enforcement action for supporting operators that target Swedish players without appropriate licences.

Responsible Gambling Framework. Sweden maintains one of Europe’s most developed responsible gambling systems. Every licensed operator must integrate with Spelpaus, the national self-exclusion register. Bonus policies are tightly controlled. Players may receive only one welcome bonus; cashback and similar offers are generally treated as bonuses under Swedish law.

Recent Changes. From 1 April 2026, Sweden prohibits gambling on credit, including credit cards, loans, and Buy Now Pay Later products.³ The government is also preparing measures aimed at offshore operators serving Swedish players. For suppliers, compliance expectations continue to increase rather than stabilise.⁶

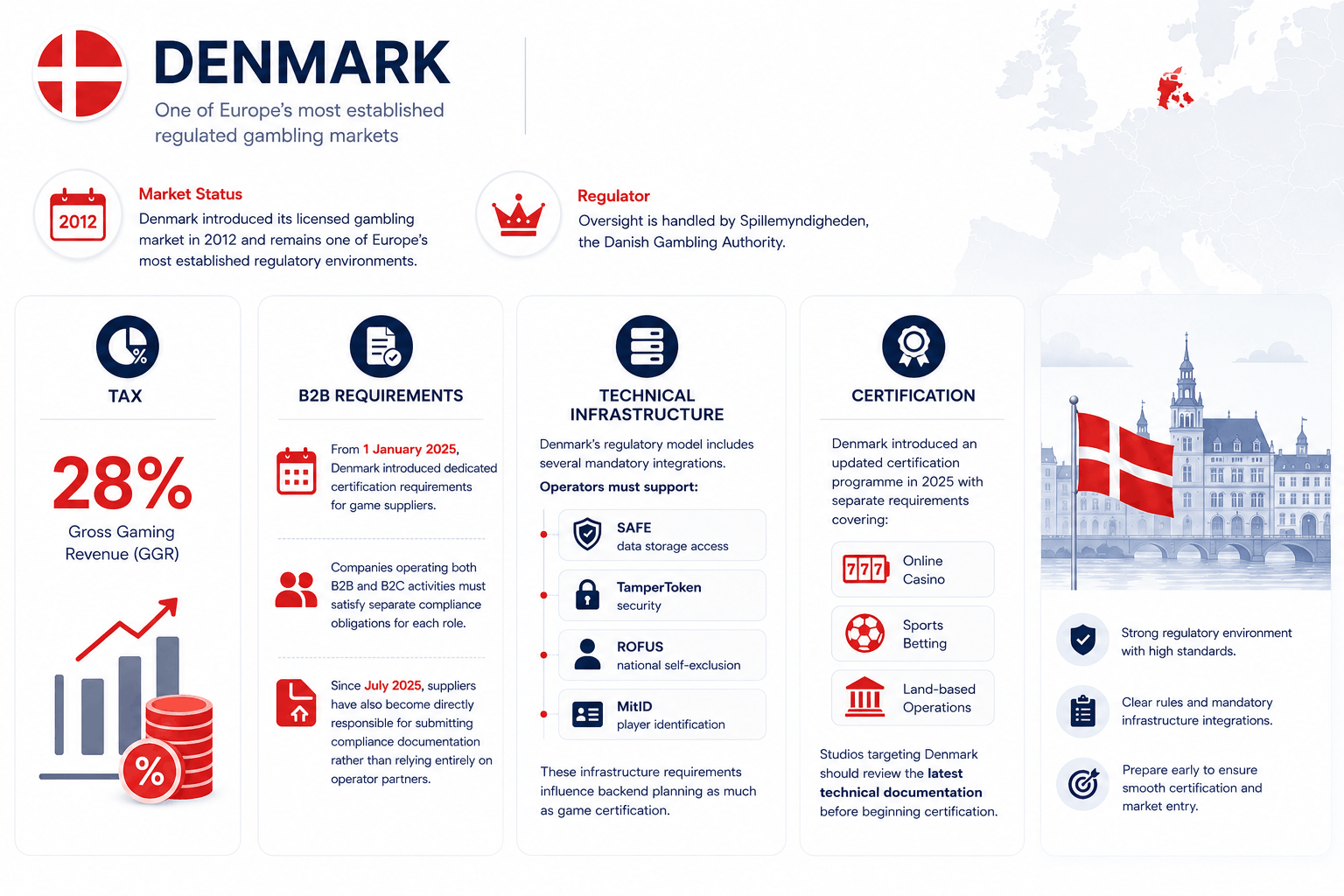

Denmark

Market Status. Denmark introduced its licensed gambling market in 2012 and remains one of Europe’s most established regulatory environments. Oversight is handled by Spillemyndigheden, the Danish Gambling Authority, under the Ministry of Taxation.⁵

Tax. 28% Gross Gaming Revenue (GGR).

B2B Requirements. From 1 January 2025, Denmark introduced dedicated certification requirements for game suppliers. Companies operating both B2B and B2C activities must satisfy separate compliance obligations for each role. Since July 2025, suppliers have become directly responsible for submitting compliance documentation rather than relying entirely on operator partners.

Technical Infrastructure. Denmark’s regulatory model includes several mandatory integrations. Operators must support SAFE data storage access, TamperToken security, ROFUS national self-exclusion, and MitID player identification. These infrastructure requirements influence backend planning as much as game certification.

Certification. Denmark introduced an updated certification programme in 2025 with separate requirements covering online casino, sports betting, and land-based operations. Review the latest technical documentation before beginning certification.

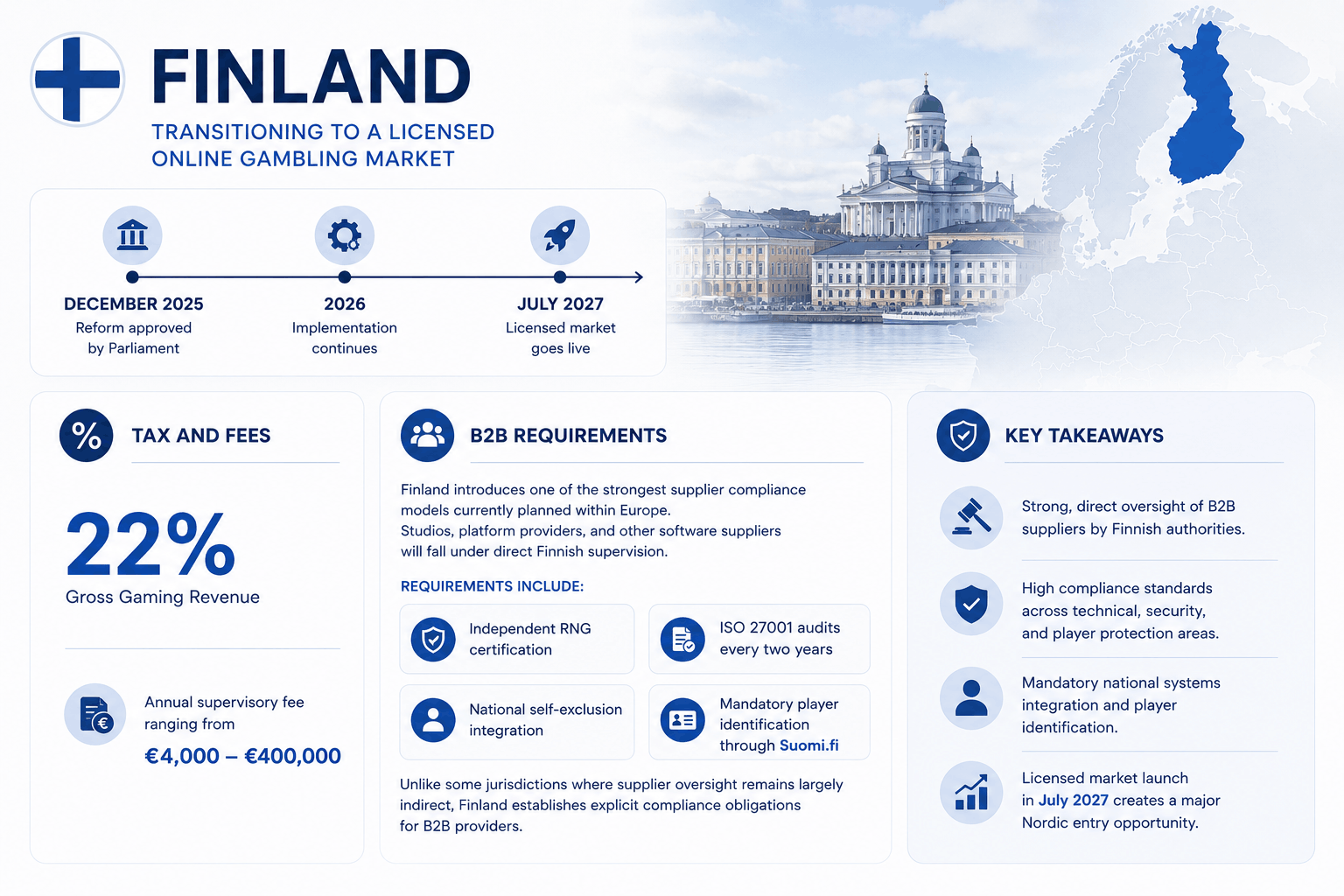

Finland

Market Status. Finland is transitioning from the long-standing Veikkaus monopoly to a licensed online gambling market. The reform was approved by Parliament in December 2025. Implementation continues throughout 2026 and 2027. Supervision is split between two ministries: the Ministry of the Interior (gambling legislation) and the Ministry of Social Affairs and Health (problem gambling).⁵ The market is currently regulated by the Gambling Administration within the Police Board, and the licence transition establishes a new regulatory agency.⁵

Tax. 22% Gross Gaming Revenue, plus an annual supervisory fee ranging from €4,000 to €400,000.

B2B Requirements. Finland introduces one of the strongest supplier compliance models currently planned within Europe. Studios, platform providers, and other software suppliers will fall under direct Finnish supervision. Requirements include independent RNG certification, ISO 27001 audits every two years, national self-exclusion integration, and mandatory player identification through Suomi.fi. Unlike jurisdictions where supplier oversight remains largely indirect, Finland establishes explicit compliance obligations for B2B providers.

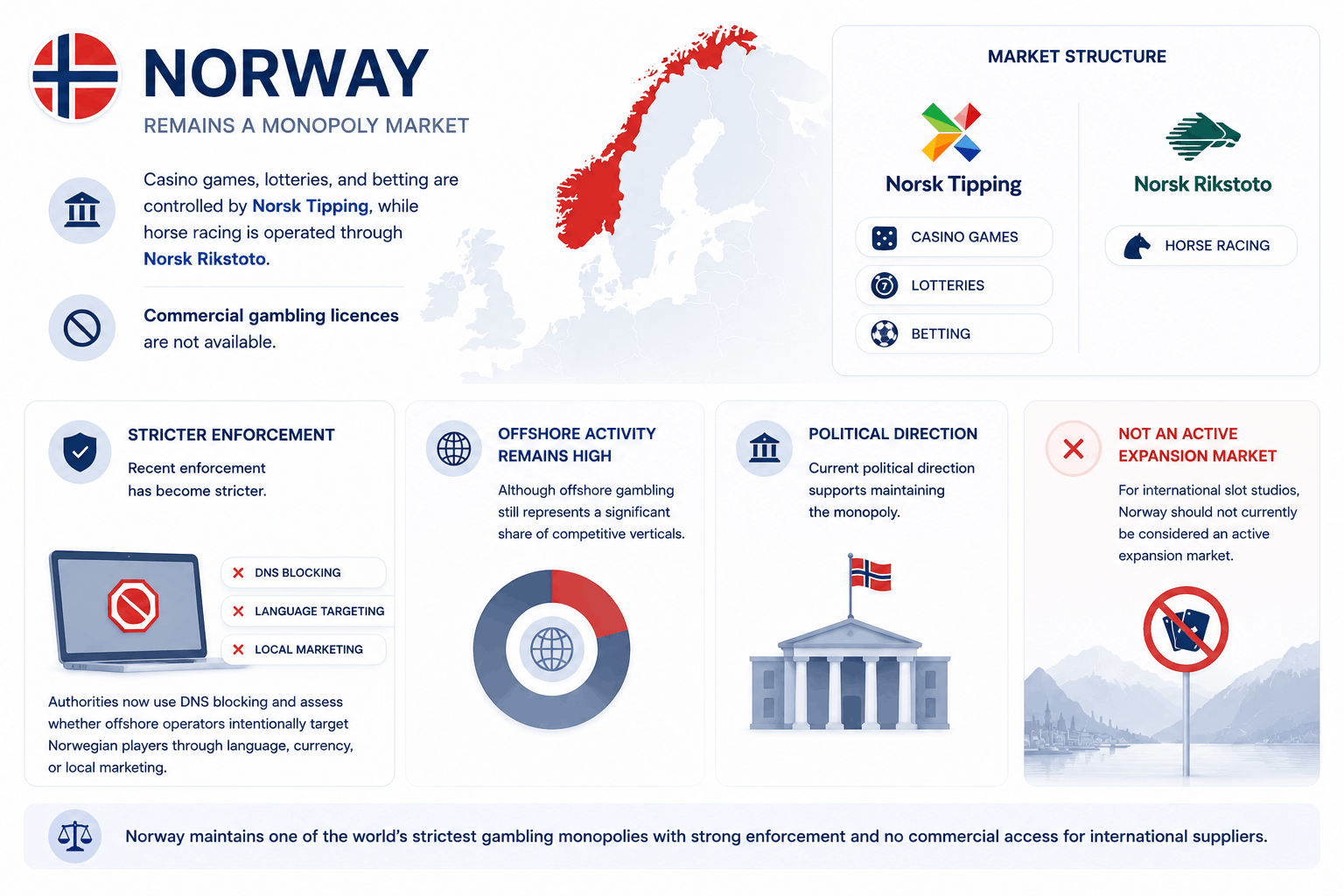

Norway

Norway remains a monopoly market. Casino games, lotteries, and betting are controlled by Norsk Tipping, while horse racing is operated through Norsk Rikstoto. Commercial gambling licences are not available.

Enforcement has become stricter. Authorities use DNS blocking and assess whether offshore operators intentionally target Norwegian players through language, currency, or local marketing. Norway defended its monopoly successfully before the EFTA Court in 2007 and has reinforced it since; current political direction supports maintaining it.⁵ Norway is not closed for now, it is a deliberate, durable monopoly. For international suppliers, it should not be considered an active expansion market.

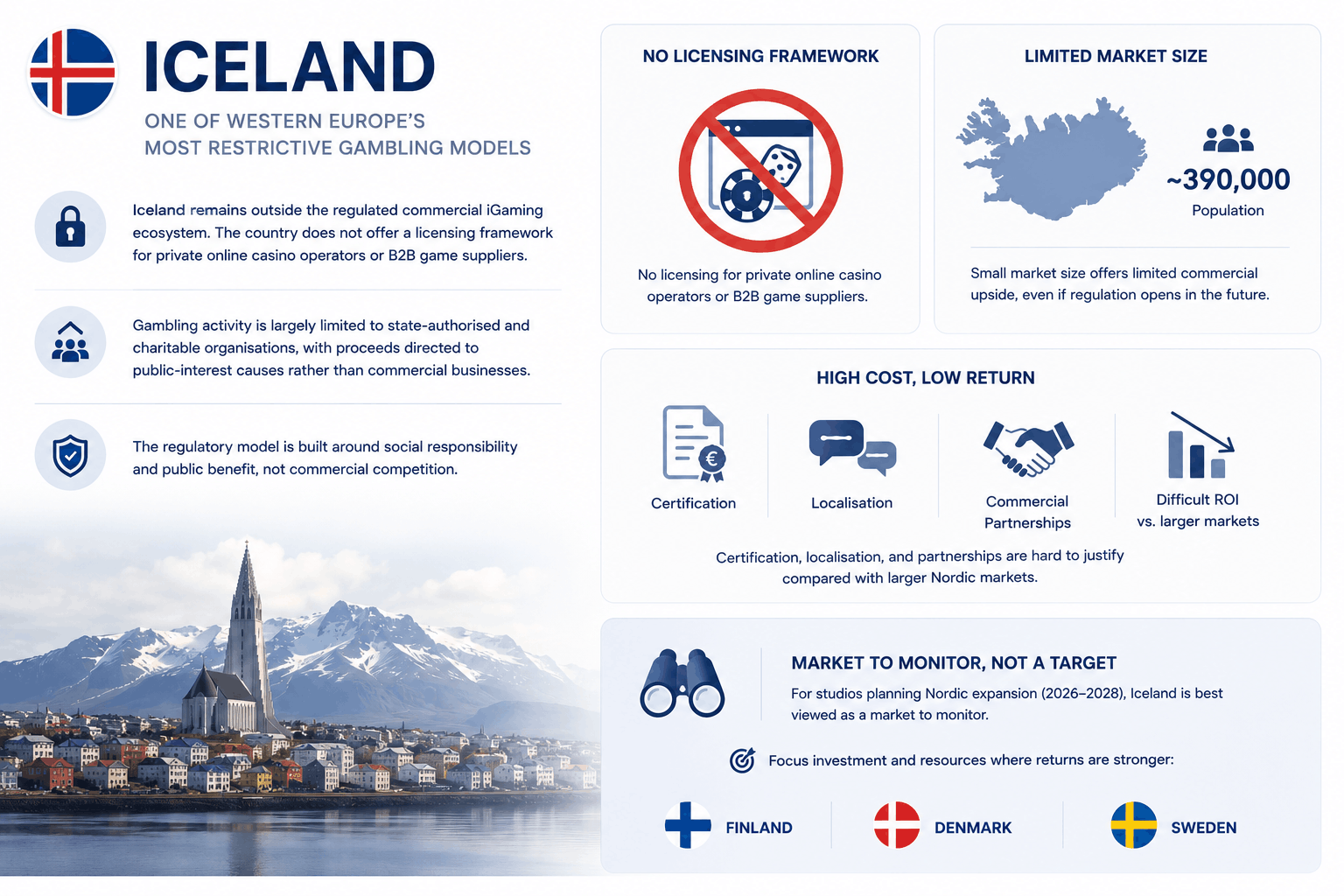

Iceland

Iceland maintains one of the most restrictive gambling models in Western Europe and remains outside the regulated commercial iGaming ecosystem. Unlike Sweden, Denmark, and soon Finland, it does not offer a licensing framework for private online casino operators or B2B game suppliers. Gambling is largely limited to state-authorised and charitable organisations, with proceeds directed to public-interest causes.

The market is also small. With a population of approximately 390,000, Iceland offers limited commercial upside even if regulation were to open in future. For most international studios, the cost of certification, localisation, and commercial partnerships would be difficult to justify against larger regulated Nordic markets. Treat Iceland as a market to monitor rather than a target for investment.

Nordic Market Comparison

| Country | Market Status | GGR Tax | B2B Supplier Requirements | Current Opportunity |

|---|---|---|---|---|

| Sweden | Licensed | 18% | Gambling software permit required | Mature, highly regulated |

| Denmark | Licensed | 28% | Dedicated supplier certification | Stable regulated market |

| Finland | Opening July 2027 | 22% | Mandatory B2B licensing from January 2028 | Highest growth opportunity |

| Norway | Monopoly | N/A | Commercial entry unavailable | Monitor only |

| Iceland | Restricted | N/A | Commercial entry unavailable | Low priority |

Production takeaway. Finland deserves the highest priority for new market entry projects. Sweden and Denmark remain attractive but mature and highly competitive. Finland offers a rare opportunity to launch into a newly licensed ecosystem while operators are actively building portfolios.

The opportunity does not reduce the preparation required: certification, compliance planning, and production workflows still need to be established before launch. Starting early provides a stronger competitive position than trying to accelerate after licensing begins.

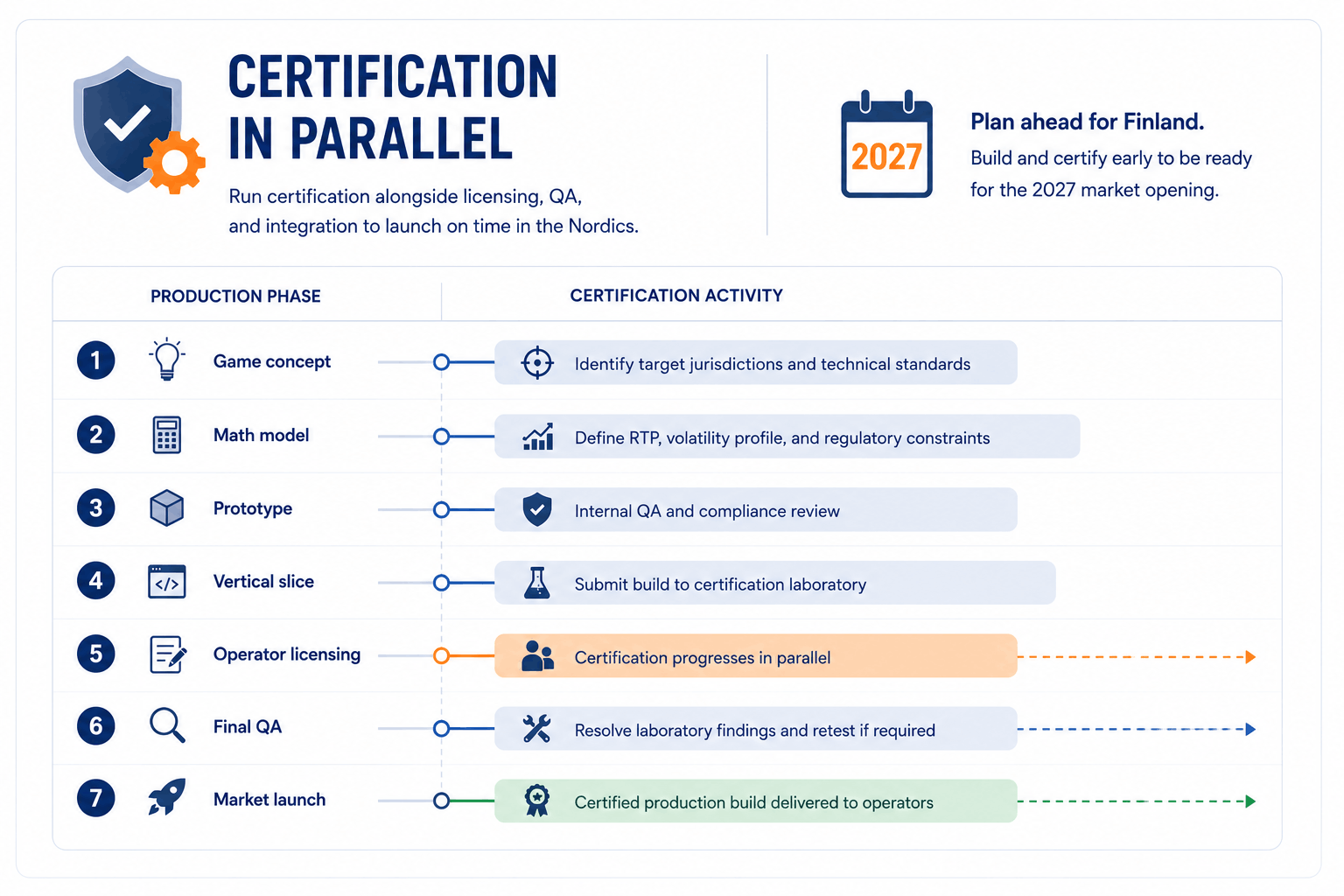

Certification and Technical Standards

Many studios treat certification as the final milestone before launch. In regulated Nordic markets, that approach creates unnecessary delays.

Certification should run alongside licensing, QA, and integration work. Waiting until development is complete can add two to three months to the launch schedule, especially if testing uncovers issues that require changes to the game’s mathematics, RTP implementation, or backend logic. For entry into Sweden, Denmark, and Finland, certification belongs in the production roadmap from the first sprint.

A practical workflow looks like this:

| Production Phase | Certification Activity |

|---|---|

| Game concept | Identify target jurisdictions and technical standards |

| Math model | Define RTP, volatility profile, and regulatory constraints |

| Prototype | Internal QA and compliance review |

| Vertical slice | Submit build to certification laboratory |

| Operator licensing | Certification progresses in parallel |

| Final QA | Resolve laboratory findings and retest if required |

| Market launch | Certified production build delivered to operators |

Running certification in parallel with licensing lets operators continue their application process while technical testing is underway. Regulators generally accept applications while certification is in progress, provided the final certificate is available before commercial launch. For Finland’s 2027 opening this sequencing is particularly important, because many operators will build launch catalogues months before the market officially opens.

Approved Testing Laboratories

Nordic regulators recognise independent testing laboratories that verify technical compliance, game fairness, and security.⁷ The approved list differs slightly between jurisdictions, but several organisations are recognised across Sweden, Denmark, and Finland.

| Laboratory | Primary Expertise |

|---|---|

| GLI (Gaming Laboratories International) | GLI-19 interactive gaming systems, full regulatory certification |

| eCOGRA | RNG testing, RTP verification, ISO/IEC 17025 accreditation, ISO 27001 audits |

| BMM Testlabs | Multi-jurisdiction certification and compliance testing |

| iTech Labs | RNG certification and technical compliance |

| SIQ (Slovenian Institute of Quality and Metrology) | Certification recognised across several European jurisdictions |

| Gaming Associates, QUINEL, TriSigma | Additional recognised testing providers for Nordic markets |

Do not select a laboratory on reputation alone. Confirm first that the laboratory is approved by every regulator you plan to target; a laboratory recognised in one jurisdiction may not automatically satisfy another. Run this check before certification begins, not after production is complete.

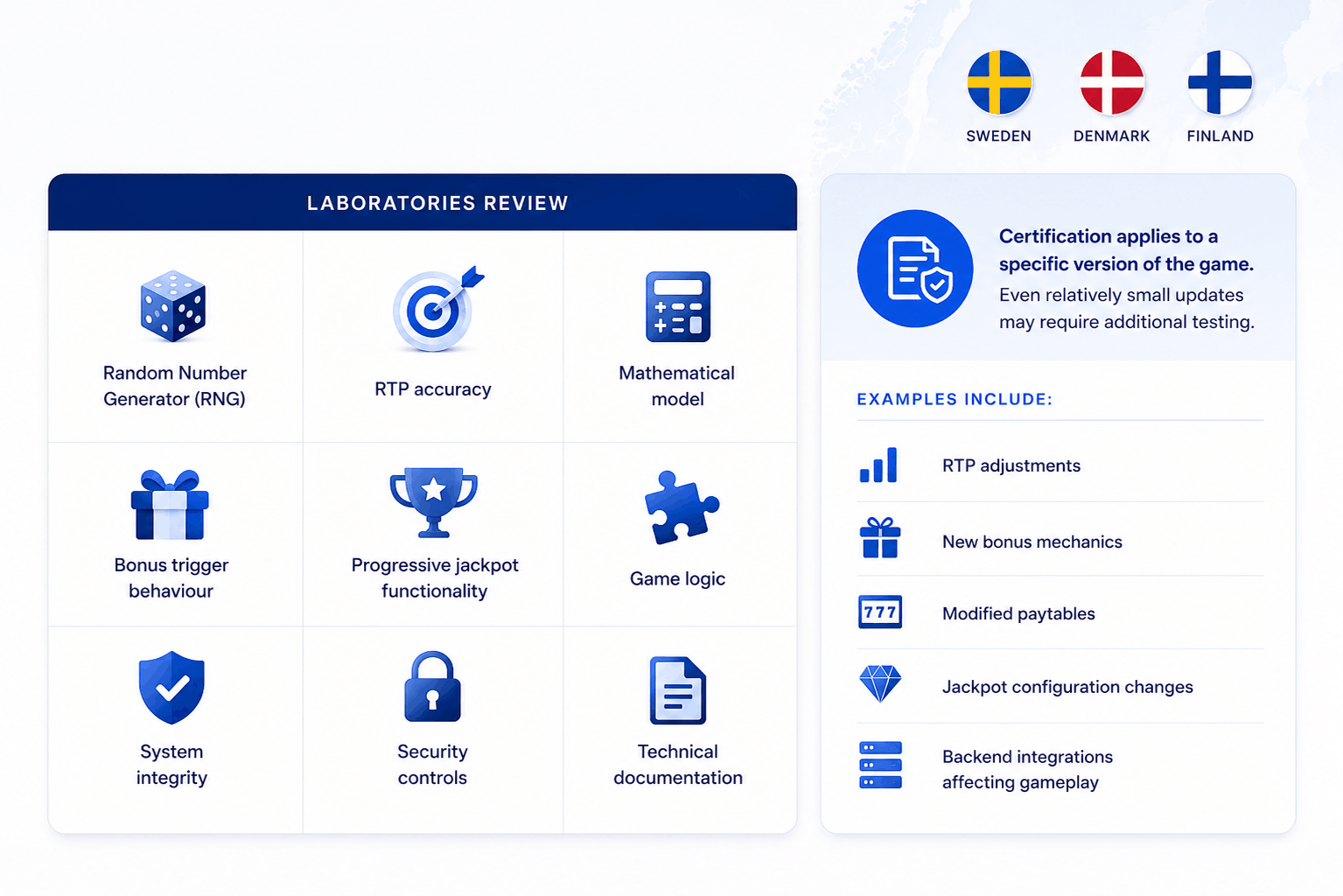

What Gets Tested

Certification covers much more than random number generation. Laboratories typically review the RNG, RTP accuracy, the mathematical model, bonus trigger behaviour, progressive jackpot functionality, game logic, system integrity, security controls, and technical documentation.

Certification applies to a specific version of the game. Even relatively small updates may require additional testing: RTP adjustments, new bonus mechanics, modified paytables, jackpot configuration changes, and backend integrations affecting gameplay. Certification is therefore an ongoing production process rather than a one-time approval. Studios planning LiveOps updates should include certification lead time in their release schedule.

Technical Standards by Country

| Country | Primary Technical Framework |

|---|---|

| Sweden | SIFS 2022:3 |

| Denmark | DGA Certification Programme, SAFE, TamperToken, ROFUS, MitID |

| Finland | ISO 27001 audits, independent RNG certification, Suomi.fi identification |

This distinction affects more than compliance teams. Backend architecture, authentication flows, audit logging, and player-protection systems all influence production planning from the beginning of development.

Why Certification Should Start Before Licensing Is Complete

Studios that wait for operator approval before beginning certification usually lose time. Experienced suppliers begin laboratory testing while licensing applications progress. Laboratory feedback arrives earlier, technical issues are identified before launch deadlines, retesting fits naturally into the schedule, and operators receive certified content sooner after obtaining licences. For Finland, where many operators are preparing initial catalogues before July 2027, earlier certification can decide whether a game appears in launch portfolios or several months later.

Design Restrictions That Change Game Specifications

Many compliance requirements cannot be added shortly before release. They affect game design, backend systems, UI behaviour, and mathematical balance from the beginning of production. Ignoring them often forces expensive redesign during QA or certification. Four areas deserve particular attention.

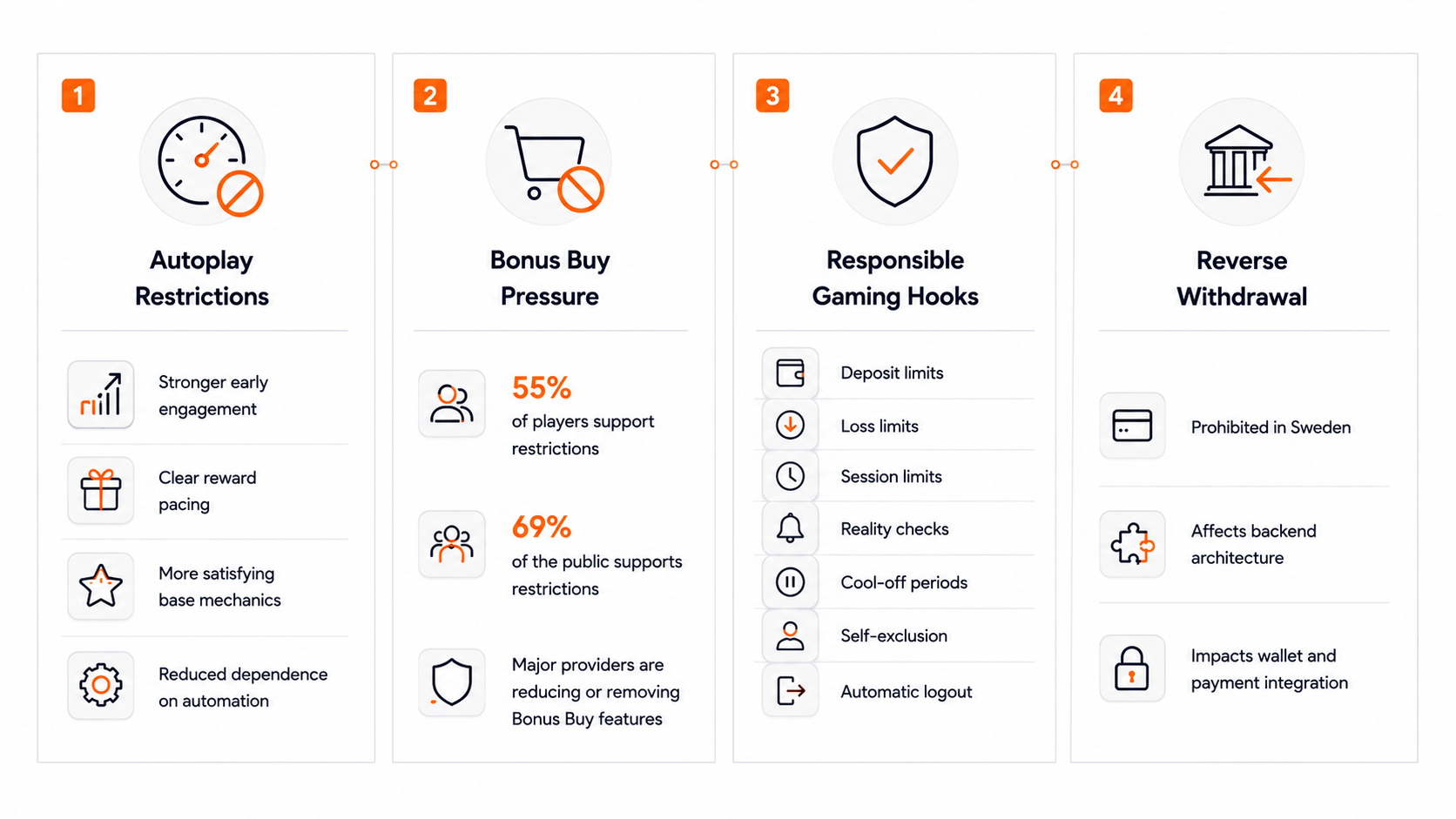

Autoplay Restrictions. Autoplay is heavily restricted in Sweden and continues to receive regulatory attention across the region.³ Without long automated sessions, the base game must remain engaging through manual play. Studios relying on repetitive autoplay loops may find session pacing feels significantly slower once autoplay is removed. The production response is stronger early-game engagement, clearer reward pacing, more satisfying base mechanics, and reduced dependence on automation.

Bonus Buy Pressure. Bonus Buy mechanics are not universally prohibited, but they face increasing regulatory and industry pressure. Industry surveys indicate that 55% of players and 69% of the wider public support restrictions.⁸ Some major providers have already adjusted strategy; Play’n GO, for example, has publicly chosen not to develop Bonus Buy functionality. Relying on Bonus Buy as the primary excitement driver introduces commercial risk. Games should remain attractive without requiring players to purchase direct access to bonus features.

Responsible Gambling Hooks. Responsible gambling features are mandatory across regulated Nordic markets: deposit, loss, and session limits, reality checks, cool-off periods, national self-exclusion systems, and automatic logout. These are often implemented through operator platforms, but games should support them without disrupting gameplay or creating UI conflicts. Planning these interactions early reduces integration work later.

Reverse Withdrawal. Sweden prohibits reverse withdrawals.³ Although this primarily affects payment systems, it influences backend architecture and wallet integration. Studios working with platform providers should account for it when defining payment-related workflows.

Nordic Design Restrictions Comparison

| Requirement | Sweden | Denmark | Finland (from 2027) |

|---|---|---|---|

| Autoplay | Prohibited or tightly restricted | Responsible gambling restrictions | Expected responsible gambling controls |

| Bonus Buy | Legal but under significant industry pressure | Increasing regulatory attention | High-risk features expected to receive greater scrutiny |

| Responsible Gambling Features | Deposit/loss limits, reality checks, automatic logout, Spelpaus integration | ROFUS integration, limits, cooling-off periods | Mandatory limits before play, national self-exclusion, player identification |

| Reverse Withdrawal | Prohibited | Not specified | Not specified |

| High-Risk Design Review | Active regulatory oversight of game design | Standard compliance review | Potential future limits on high-risk mechanics |

Compliance by design. The strongest theme across Nordic regulation is that compliance should be designed into the product rather than added during certification. That means considering regulation during game design, mathematical modelling, backend planning, UI design, QA, and certification. Waiting until the final production phase usually increases both cost and development time.

Before writing the first line of production code, answer five questions: Can the game maintain engagement without autoplay? Does the base game remain satisfying without Bonus Buy? Are responsible gambling interruptions supported naturally? Does the backend support national identification and self-exclusion systems? Can future updates be certified efficiently? These shape the production roadmap as much as art style or feature selection.

What Nordic Players Expect from Slot Games

Understanding the Nordic Player

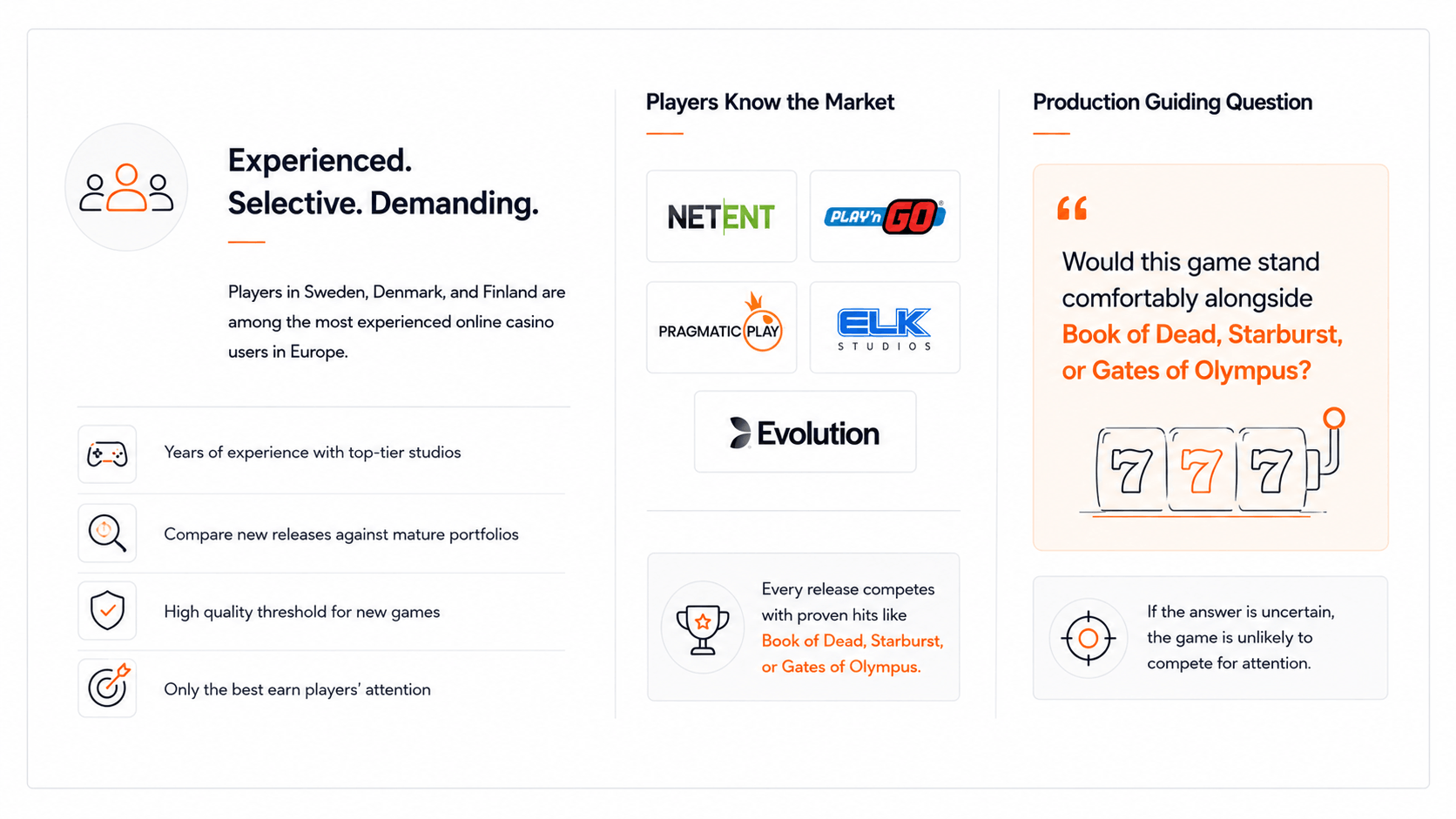

Players in Sweden, Denmark, and Finland are among the most experienced online casino users in Europe. Most have played products from NetEnt, Play’n GO, Pragmatic Play, ELK Studios, and Evolution for years, and compare new releases against mature portfolios rather than against new entrants. This creates a high quality threshold: a game that performs in less mature markets may struggle in Nordic lobbies if its mathematics, pacing, or presentation feel outdated.

Every production decision should answer one question: would this game stand comfortably alongside Book of Dead, Starburst, or Gates of Olympus? If the answer is uncertain, the game is unlikely to compete for attention.

RTP Remains an Important Decision Factor

Unlike casual markets where players rarely inspect game details, Nordic players often check RTP. The research points consistently to an expectation of 96% or higher. Not every successful title shares the same RTP, but transparency matters, and players compare titles before choosing where to spend longer sessions. Consider RTP during early mathematical planning rather than adjusting it late.

Medium Volatility Performs More Consistently

The strongest long-term performance tends to come from medium-volatility games that balance regular wins with meaningful bonus potential. Extremely volatile mathematics creates longer losing streaks and greater dependence on rare events, a profile that aligns less closely with Nordic preferences under increasingly strict responsible gambling regulation. Many studios now design mathematics with several levels of excitement within one game rather than a single rare jackpot event, supporting longer sessions while maintaining engagement.

Mechanics That Continue to Perform

These are no longer novelties; they are the baseline expectation for modern premium slots.

- Megaways — variable reel layouts; every spin creates different winning opportunities.

- Cluster Pays — adjacent-symbol wins that support cascading mechanics naturally.

- Cascading / Avalanche Reels — winning symbols disappear and new ones fall in, allowing multiple consecutive wins; strong when combined with progressive multipliers.

- Ways-to-Win Systems — 243, 1024, and expanding ways; simplify gameplay while increasing perceived variety.

- Walking and Expanding Wilds — extend excitement across multiple spins without aggressive mathematical profiles.

- Collection Mechanics — players collect symbols or tokens that unlock stronger features, rewarding continued play without depending on rare outcomes.

Mechanics That Present Greater Risk

Bonus Buy dependence. Games that rely heavily on purchased bonus access become vulnerable as regulatory pressure increases. Players should enjoy the complete experience without buying direct entry into bonus rounds.

Extremely volatile mathematics. Large maximum wins alone do not guarantee commercial success. Very long losing streaks reduce engagement among experienced players seeking balanced entertainment. Favour sustainable session design over maximum advertised payouts.

Art Direction and Visual Trends

Norse mythology continues to lead. Vikings, Ragnarök, Odin, Thor, Loki, and mythical creatures remain culturally relevant throughout the region. Execution, not theme, is now the differentiator.

Mythology 2.0. A defining 2026 visual trend. Earlier mythology slots presented gods through bright cartoon artwork; recent premium productions shift toward cinematic presentation, realistic lighting, darker palettes, dramatic storytelling, and high-detail characters. Successful mythology games increasingly resemble fantasy illustration rather than traditional casino artwork. The trend extends beyond Norse themes into Egyptian, Greek, Aztec, Mesopotamian, and Polynesian mythology.

Premium illustration stands out. Lobbies are visually crowded, with many games sharing layouts, icon styles, and palettes. Hand-crafted illustration attracts attention more effectively than generic vector graphics, creating a stronger first impression during browsing. For studios investing in new IP, illustration quality can matter as much as feature design.

Mobile-first production. Portrait-oriented layouts continue to gain momentum. Many modern productions begin with mobile composition and scale upward, influencing symbol readability, button placement, animation timing, UI hierarchy, and bonus presentation.

Console-level visual expectations. Players increasingly compare casino games with the broader games industry. Studios have adopted console-style techniques: cinematic lighting, dynamic shadows, high-detail materials, richer environmental animation, and reactive effects. HTML5 remains the deployment platform, but production quality increasingly reflects Unreal Engine 5 and Unity workflows.

Diegetic UI. Modern interfaces integrate controls into the game world: a compass as the spin button, treasure chests triggering bonuses, animated environmental indicators replacing traditional HUD elements. This reduces clutter and strengthens immersion.

AI within the art pipeline. AI-assisted production is a practical workflow, not a finished product. Studios use generative tools for early concept exploration, background variations, composition studies, and colour experiments; final assets, premium symbols, and art direction remain under human supervision.

Benchmark: Providers Setting the Standard

| Provider | Why It Matters |

|---|---|

| NetEnt | Long-established Swedish provider known for polished presentation and broad range. Reference titles: Starburst, Gonzo’s Quest. |

| Play’n GO | Strong production quality and gameplay balance. Book of Dead is a defining regional title. Has avoided Bonus Buy mechanics. |

| Pragmatic Play | Large, consistent portfolio with modern mechanics. Gates of Olympus demonstrates current mythology presentation. |

| ELK Studios | Boutique visual identity with distinctive animation. |

| Hacksaw Gaming | Strong mobile-first approach and recognisable art direction. |

| Evolution | Dominant live-casino provider shaping premium-presentation expectations across lobbies. |

Reference Titles Worth Studying

| Title | Production Lesson |

|---|---|

| Starburst | Clear rules, approachable mathematics, strong visual identity. |

| Book of Dead | Recognisable theme, effective Free Spins, excellent mobile readability. |

| Gonzo’s Quest | Cascading reels integrated naturally into the core loop. |

| Gates of Olympus | Modern cinematic mythology with multiplier progression. |

| Mega Moolah | Long-term engagement driven by progressive jackpots. |

| Hall of Gods | Network jackpot structure combined with mythology. |

A Practical Five-Step Market Entry Plan

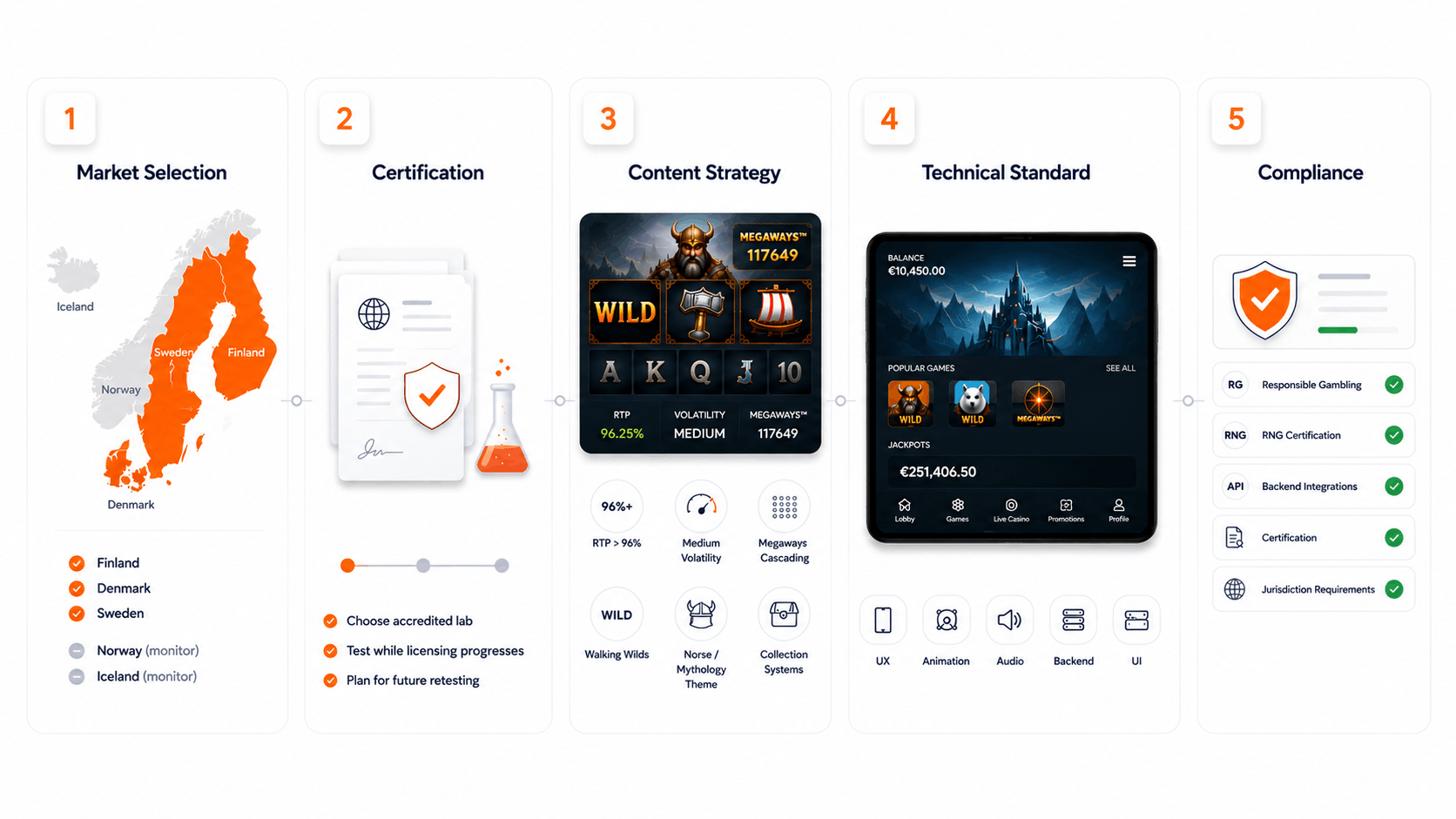

Step 1. Prioritise markets. Focus on Finland, Denmark, and Sweden. Treat Norway and Iceland as monitoring markets, not immediate targets.

Step 2. Start certification early. Select a laboratory recognised across your target jurisdictions. Begin testing while operator licensing progresses. Budget for retesting as part of LiveOps.

Step 3. Build content around regional preferences. Successful Nordic portfolios combine Norse or cinematic mythology, premium illustrated art, RTP above 96%, medium volatility, Megaways or cascading mechanics, Walking Wilds, and collection systems, without depending on autoplay or Bonus Buy.

Step 4. Match the technical standard. Modern Nordic releases expect mobile-first UX, premium animation, cinematic presentation, adaptive audio, immersive UI, and polished backend integration. Visual quality is now a competitive requirement, not a differentiator.

Step 5. Treat compliance as part of production. Responsible gambling features, certification, backend integrations, and jurisdiction-specific requirements belong in the original specification. Compliance added near launch usually increases cost and delays delivery.

Honest Risk Assessment

Nordic expansion offers attractive opportunities, but the barriers are significant. Certification, B2B licensing, ISO 27001 audits, and ongoing retesting require budget and production capacity.

Competition is demanding. Sweden and Denmark are relatively small markets that nonetheless host some of the industry’s strongest suppliers. New entrants compete directly with NetEnt, Play’n GO, Pragmatic Play, ELK Studios, and Hacksaw Gaming.

Regulation continues to evolve. Sweden has introduced progressively stricter measures, including the 2026 credit gambling ban. Finland’s implementation will keep developing after the market opens, particularly through the transition to mandatory B2B compliance in January 2028. Studios whose strategy depends heavily on Bonus Buy should reassess their roadmap; as scrutiny increases, games with strong standalone gameplay are likely to prove more resilient.

The strongest opportunity lies in focused execution rather than broad expansion. For many studios, entering Finland with two or three well-produced, fully certified mythology titles may deliver greater long-term value than simultaneous launches across multiple jurisdictions.

Closing Perspective

Nordic regulated markets reward preparation. Certification, responsible gambling requirements, production quality, and mathematical design all influence commercial success well before launch. Finland’s licensing reform creates a rare opportunity for those who prepare ahead of the market opening rather than after it.

At Twin Win Games, we build casino content with regulated-market requirements considered from the first production sprint. If you are evaluating Finland or broader Nordic expansion, we would be glad to discuss production planning, certification strategy, or developing content designed for regulated markets from day one.

Data current as of June 2026. Regulatory frameworks continue to evolve. Verify legal and technical requirements before committing to market entry, particularly in Finland, where implementation is ongoing.

Sources

- Offshore spend of €520–590M/year and the ~50% online share: IMGL Magazine, “Finnish Gambling Reform: First Regulatory Steps Towards Liberalization.” https://www.imgl.org/publications/imgl-magazine-volume-3-no-1/finnish-gambling-reform-first-regulatory-steps-towards-liberalization/ — corroborated by Nikkinen, J. / Nordic Welfare Centre (POPNAD), “Renewal of the Finnish gambling legislation,” citing the Finnish Consumer and Competition Authority (KKV, 2023). https://nordicwelfare.org/popnad/en/artiklar/renewal-of-the-finnish-gambling-legislation/

- European Gaming (2026), “Finland receives 50 licence applications ahead of 2027 iGaming market launch.” https://europeangaming.eu/portal/latest-news/2026/06/10/206617/finland-receives-50-licence-applications-ahead-of-2027-igaming-market-launch/

- iGaming Business, “Sweden to ban autoplay and reverse withdrawal.” https://igamingbusiness.com/legal-compliance/regulation/sweden-ban-autoplay-reverse-withdrawal/

- Helsinki Times, “Nordic slot themes dominate 70% of top-played games in Finland.” https://gambling.helsinkitimes.fi/blog/2025/06/09/nordic-slot-themes-dominate-70-of-top-played-games-in-finland/

- Thompson, C. F. (2025). Comparing Gambling Policy Evolution in Denmark, Finland, Norway, and Sweden. International Journal of Public Administration, 48(5–6), 395–406. https://doi.org/10.1080/01900692.2025.2470760

- SBC News, “Sweden painted as leader in Nordics gambling transformation.” https://sbcnews.co.uk/europe/2024/04/02/sweden-painted-as-leader-in-nordics-gambling-transformation/

- UK Gambling Commission, approved test houses. https://www.gamblingcommission.gov.uk/licensees-and-businesses/guide/page/approved-test-houses

Related Services from Twin Win Games

For studios building a full Nordic catalogue, here is the complete production scope Twin Win Games covers:

- Casino Game Development — slots, table games, instant games, crash

- Slot Game Development — full-cycle slot production for regulated markets

- Slot Game Art — premium illustrated art, mobile-first symbol design

- HTML5 Game Development — cross-platform delivery for all aggregation platforms

- Backend Game Development — architecture for SAFE, TamperToken, ROFUS, and Suomi.fi integrations

- Game Engine — proprietary engine with pre-built integrations for Relax, Yggdrasil, and Aristocrat

- Crash Game Development — provably fair multiplayer crash for mobile-first markets

- Roulette Game Development — HTML5 roulette for regulated casino lobbies

- Blackjack Game Development — certified blackjack for European market entry

- Baccarat Game Development — baccarat for premium and VIP-segment operators

- Poker Game Development — video poker and table poker for licensed markets